Twist Bioscience: Silent partner in the new era of biology

How DNA synthesis powers the infrastructure for writing biology

Hi friends 👋

Welcome to Health & Wealth — your weekly source of the latest health research and biotech trends. While genomics stocks have been ruthlessly plummeting, I’ve been patiently researching and thinking deeper about innovative technologies at their inflection point, with the potential to shape our future biological world. If you are new, you can join here — feedback is encouraged and welcome.

Article Highlights

Twist Bioscience TWST 0.00%↑ aims to be the pick-and-shovel provider of synthetic DNA to power the future of bioengineered products. They’ve built a technology platform that miniaturizes and automates known chemistry to write DNA cost-effectively and at scale.

Exponential drops in synthesis cost introduce challenging market dynamics because more volume is needed to make the same topline revenue. Diagnostics and therapeutics are near-term areas where Twist’s model can shine.

Emerging diagnostics such as liquid biopsy for cancer detection is a unique opportunity for Twist because large volumes of custom probes are needed and the components of tests are set after receiving FDA clearance.

In drug discovery, Twist productized their antibody libraries which can be licensed out to companies. This gives them pricing power and the ability to share value creation through milestones and royalties.

Synthetic biology emerged last fall with much fanfare when Ginkgo Bioworks went public, but Twist Bioscience is an underappreciated player providing the infrastructure for writing biology. Here we’ll be exploring the question: how can we make DNA as easy as it is to read it?

At its core, Twist Bioscience (TWST) is a DNA factory designing and mass-producing genetic material from scratch. Their customers use synthetic DNA in many ways — to create new organisms, sequence specific areas of the genome, discover novel drug candidates, and develop alternative forms of digital data storage.

As these industries continue to grow and mature, Twist aims to be the dominant pick-and-shovel provider of synthetic DNA to enable their customers’ success. Wherever the science and commercial applications go, Twist is the silent partner and proxy for the research, discovery, development, and production of bioengineered products.

Twist wasn’t always the market leader — in 2013, they were newcomers to a market that many thought was already saturated and commoditized. But they saw something different: “a big market with unhappy customers.” Because making synthetic DNA was prohibitively expensive and slow, users could only test a few designs before needing to abandon ideas. This was a bottleneck to enabling modern synthetic and molecular biology, which needs to test thousands of sequence variants at once and thus, requires high volumes of synthetic DNA.

Twist’s technological advantage was miniaturizing and automating known chemistry for efficiently writing DNA. Instead of conducting chemical synthesis of DNA in traditional 96 well plates to produce one piece of DNA per well, they engineered the same process on a silicon chip that could now print millions.

The result: an ultra-high throughput DNA synthesis platform that reduces high-cost input materials by 99.8%, increases throughput by 10,000x, and cuts the cost per base pair to cents rather than dollars.

In many ways, the story of DNA synthesis resembles that of sequencing — taking an existing fundamental reaction (phosphoramidite chemistry and Sanger sequencing, respectively) and massively parallelizing it to increase volume. From the Giant of Genomics, Illumina:

“The critical difference between Sanger sequencing and NGS [next-generation sequencing] is sequencing volume. While the Sanger method only sequences a single DNA fragment at a time, NGS is massively parallel, sequencing millions of fragments simultaneously per run. This process translates into sequencing hundreds to thousands of genes at one time.”

But this type of “better, cheaper, faster” exponential strategy can make you vulnerable to getting displaced by another differentiated technology that improves faster. Hindsight is 20/20, but 15 years ago, it was quite unclear who would emerge as the sequencing market leader. It got me thinking about the durability of Twist’s business, which boils down to two fundamental questions:

Do they have a sustainable and defensible advantage to be the dominant service provider for synthetic DNA?

How much value can they capture in the products their customers build?

To unpack Twist’s ability to manifest itself as the de facto infrastructure layer of writing biology, we need to understand the game at play:

What can synthetic DNA be used for?

Revenue from R&D vs. production

Switching costs: why getting in diagnostic tests early matters

Network effects: creating better products given more customers

Scale: Twist’s leading advantage

DNA synthesis as a service or product?

What can synthetic DNA be used for?

Twist’s future potential critically depends on the demand for synthetic DNA. So what do their global customer base of ~2,900 customers use synthetic DNA for?

They’re currently focused on 4 core markets:

Synthetic biology is where they got their start — synthetic genes can be inserted into organisms to make functions or ingredients that wouldn't otherwise be produced.

NGS tools make up over 50% of total revenues — diagnostic tests often require DNA probes that function like magnets binding to sequences of interest in a sample.

Biopharma is a recent fast-growing division — antibody libraries consisting of many different sequence variations help with the discovery and optimization of new drug candidates.

DNA data storage is a long-term “moonshot” goal — archiving data in DNA can be a compact, durable solution to meet the demand of exponential data storage needs.

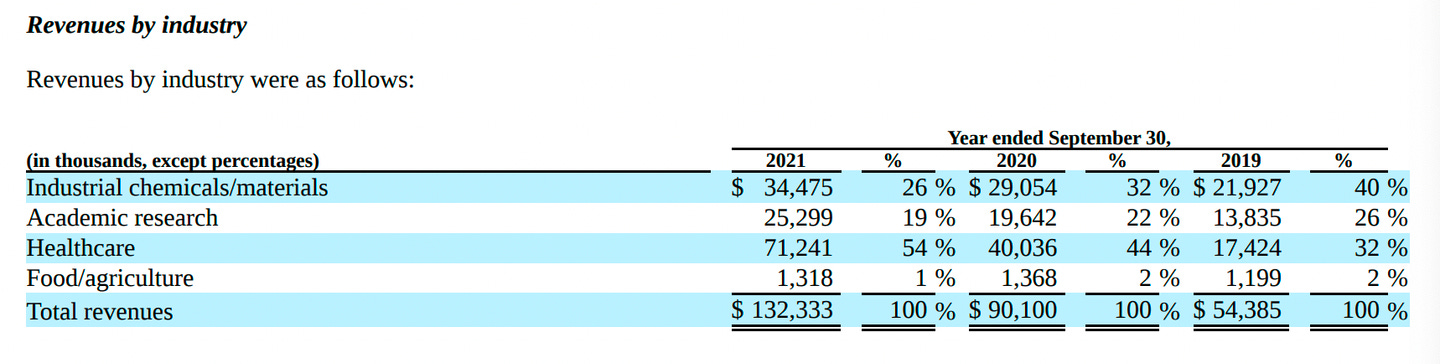

Before researching, I had a false notion that Twist is a “synbio company.” But synthetic genes are actually their slowest growing segment at a 21% compound annual growth rate over a two-year period. What caught me even more by surprise was how NGS tools make up more than 50% of total revenues:

We also see when segmenting by industry, healthcare makes up over half of their revenue while other industries have remained stagnant or tapered relative to overall revenue growth:

Revenue from R&D vs. production

In hindsight, the shift from industrial synbio to diagnostics and therapeutics makes sense. A major limitation of supplying DNA for synthetic biology is once a sequence is finalized and embedded into the organism, there’s no need for more synthetic DNA. The modified organism becomes its own copy machine, growing and reproducing.

So while it’s impressive that Ginkgo ordered ~1 billion DNA bases in 4 years from Twist with expectations for ongoing large orders, the synthetic biology market is still relatively small. Twist’s potential here is capped by only being able to participate in R&D, not scale-up and production. As a result, the value capture of their customer’s products is limited.

In contrast, for diagnostic tests, each patient sample processed uses DNA probes. So as Twist’s customers increase commercial test volume, their revenue increases proportionately. Same thing with biopharma:

"The great thing about cell engineering is that you need a lot of custom DNA. If every patient gets a different engineered cell, then the genetic material payload needs to be made for each patient... We can then participate in production mode.”

[Q3 2021 Earnings Call: CEO Emily Leproust]

This is also reflected by how they view where the future big market drivers to be — liquid biopsy, drug discovery, and archival storage:

So while I don’t discount their position as a leading provider of synthetic genes, it’s also unlikely to be their biggest market opportunity. The rest of this piece will focus on diagnostics, biopharma, and beyond.

Switching costs: why getting in diagnostic tests early matters

First, some context on what “NGS sample prep tools” means:

If you think of your genome as a book, genetic tests rarely read through the whole book. Instead, they extract relevant excerpts. That’s essentially what “targeted enrichment” using DNA probes does.

But cherry-picking sequences of interest can be tricky — you can either lose information because probes fail to properly bind to the DNA sample or introduce bias when amplifying:

NGS sample prep is a mature field, but Twist’s value proposition here is that they can synthesize cheaper, more accurate, and rapidly customizable probes. Custom panels account for 80% of their NGS revenue.

Cancer liquid biopsy is an early opportunity for Twist

Target enrichment is taken to a logical extreme when screening for cancer from a blood test (liquid biopsies). Here, you’re detecting if pieces of tumor DNA circulating in the bloodstream are present. Because circulating tumor DNA represents such a tiny fraction (0.01-1%) of total cell-free DNA, it’s equivalent to finding a needle somewhere on a football field.

Large panels of custom DNA probes are therefore vital to pull out and amplify the relevant information — something that Twist does really well, quickly and cost-effectively.

But the key here is that liquid biopsy for early cancer detection or recurrence monitoring is still nascent, with many companies still in the development and clinical trial phase. Twist wants these companies to be their customers early on because once they receive clearance from the FDA, the components of the tests — including sample prep — are set for the foreseeable future, and changing vendors isn’t worth the regulatory hassle. As a result, these customers are incredibly sticky.

The market for disease research estimates would be $19.6 billion by 2025. While we do not develop liquid biopsy tests ourselves, we estimate that the DNA portion is approximately 5% to 10% of the total market, adding $1 billion to $2 billion of serviceable market to Twist. Our liquid biopsy customers are at various stages of development, both in their own drive towards commercialization and in their use of Twist products. Some are just starting to create test and piloting our products, others have completed the design and product specification including our NGS products and are conducting clinical studies, and a few of them are already commercial.”

[Q1 2022 Earnings Call: CEO Emily Leproust]

Twist currently works with over 20 companies developing liquid biopsy tests. GRAIL is one such customer — an early prototype of their screening test relied on 100,000 capture probes designed for specific cancer DNA mutations and more than 1 million capture probes to target methylation changes.

The bottomline: Their aggressive execution to gain market share in emerging diagnostic tests reflects their understanding that “if we weren’t in the pilot, even if our product was better [than competitors] if we came in 12 months later, we would have a very low shot of getting into those tests.”

Network effects: creating better products given more customers

Drug discovery is notoriously challenging, time-consuming, and expensive. Twist plays a part by providing comprehensive antibody libraries to increase the chance of finding high-affinity binding antibodies. Each library contains over 10 billion human antibody sequences — like different configurations of colored beads strung together:

What’s valuable here is that Twist positioned itself as a software platform that can be licensed out to companies designing antibodies. This gives them pricing power and the ability to share value creation through milestones and royalties:

“Average value of an antibody is $50 million/base and we’re selling it for 9 cents a base, so there’s a lot of value in between... so we built a drug discovery optimization engine to go sell this as a service... This year we raise our price. No one batted an eye and now more than 50 partnerships have milestones.”

[Cowen Healthcare Conference 2022: Emily Leproust]

Creating customized tools for their biopharma customers improves Twist’s libraries over time, which can be productized and sold to other customers. Productization of their service is very important because Twist can gain new customers with substantially less customized build-time on their end. Having a track record of quality data sets also spins the flywheel, compounding more proof points and attracting new (previously skeptical) biopharma customers.

Some closing thoughts

Twist Bioscience is a promising business that has displayed aggressive short-term execution with long-term strategic thinking in mind. They seek areas where there’s a market for DNA synthesis and use their platform technology to take market share quickly.

Scale remains their leading advantage, which is particularly well-suited for diagnostics and therapeutics development and production needs. However, they’re still a few years away from achieving breakeven operations, and investors should expect further dilution on the path there.

There is more I planned on discussing here, including how emerging enzymatic DNA synthesis companies might change the market landscape, but this post is already quite long. I may extend this piece to part 2 in the future. If you're new, subscribe so you don't miss it:

Part 2 is now published. Thanks for reading!

Christina

Great work Christina! Two other broad points you might consider are, firstly, the many attractive markets continually opening up for TWST eg CRISPR screening, MRD, bispecific MaB, etc and secondly, the calibre and quality of management. Also, there is a huge tailwind when price reduction in sequencing pushes up volumes. Sequencing and synthesis are joint in the hip.